The Asia-Pacific spa market today is dominated by luxury and upscale facilities, but the growth in the market will come from young and first-time visitors who are interested in complementary and holistic services that reflect regional traditions.

The Tourism Observatory for Health, Wellness and Spa (TOHWS), in cooperation with Resources for Leisure Assets, published its 5th benchmarking report on the role of spa and wellness facilities in tourism, and this year took a close look at the Asia-Pacific region, with the help of the Asia Pacific Spa and Wellness Coalition.

The survey results reveal that the spa market is still dominated by luxury/upmarket facilities in the Asia-Pacific region, and 65 per cent of the market considers itself a luxury operator, compared to 55 per cent of spa and wellness facilities globally.

Demographics

We can observe a different age distribution of guests when we look at the Asia-Pacific region compared to our global data, with Gen Y making up the largest percentage of guests (29 per cent, vs 20 per cent globally), followed by Gen X (26 per cent, compared to 25 per cent globally). In the rest of the world, Baby Boomers may lead the charge when it comes to spas, but in Asia, they come in third – topping only those born before 1946 and Gen Z, born between 1996 - 2012. This has important implications for both spa design and programming.

Data also show that although the female segment is still the typically dominant one in Asia – women make up around 60-65 per cent of the share of total guests – the importance of male guests is growing. Several spa and wellness centres report the number of male and female guests is equal, and a few reported more male than female guests.

The role of international guests is significant in the region since more than 50 per cent of guests are registered as international visitors, with most of those (60 per cent) coming from Europe.

What motivates guests?

The main motivation of foreign guests remains treatments and services, followed by the brand and reputation of the spa or wellness facility. We offered a long list of likely motivation triggers to choose from. The data we received both in the pilot and in the follow-up survey suggest that technology, design or price play little role in foreign guests’ motivation in selecting a spa or wellness facility – important information since investors tend to spend a significant amount on spa design and technology.

Operators also confirmed the growing trend of social consumption – when treatments and services are consumed in small groups, rather than individually. This suggests that single women should no longer be considered the number one segment for spa and wellness services, and has a direct impact not only on spa operations but also on spa and wellness space design, service zoning and allocations, as well as guest journeys.

It should be noted that demand appears to be more and more fragmented as we compare different regions around the world. Operators need to define relevant market segments differently, depending on the country they are targeting. Global marketing and branding does not seem to be working anymore.

What treatments do guests want?

In terms of popularity of services and treatments, we asked operators to identify such services by different guest groups, i.e. walk-in guests, domestic guests who are visiting and foreign guests. Whereas the global data show the importance of natural resources-based therapies and treatments as well as services based on local resources, the Asia-Pacific market shows a somewhat different path.

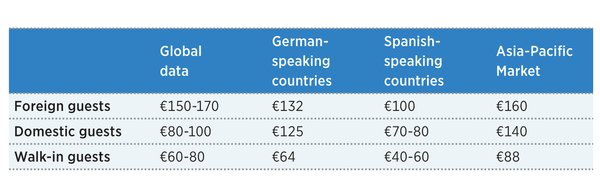

Not surprisingly, there is a high demand for complementary and alternative therapies and holistic treatments in Asia, which reflects the rich spiritual and holistic resources and traditions. This is actually not that different from the global data, however; holistic and traditional healing practices very much fall under the ‘local resources’ category. The only difference is how these are to be marketed – either as holistic, complementary services or local resources. The spending patterns do not differ greatly from that of the global data. Foreign guests are estimated to spend approximately €160 per day on spa and wellness services.

In terms of market potential and growth prospects, developers and operators need to look at their respective markets in detail. We can observe rather diverging trends and forecasts depending on which market we look at. The only converging market data is that foreign travellers will look more and more for healthy services and options during their travels. This interest may not turn these guests into wellness tourists, but clearly shows the way in which market demand is moving.

Spas and wellness facilities must apply special marketing and management measures if they want to achieve a healthy mix of walk-in, domestic and foreign guests. The current and forecasted demand from these major groups shows limited overlap, and this provides challenges in operations and communication.

The operators in the Asia-Pacific region reported a mixed growth data for 2017.

• The number of walk-in guests grew by 10 per cent

• The amount of domestic visitors changed by less than 5 per cent, whereas

• The number of foreign tourists was stagnant.

It was interesting to observe that the number of first-time customers and number of treatments sold grew by 5-10 per cent from walk-ins and from domestic markets.

Growth projections

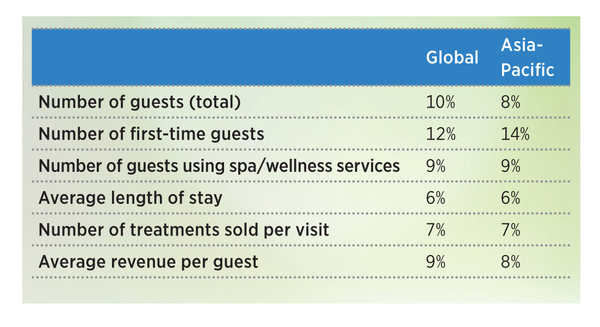

In terms of forecasted market changes for 2018, the Asia-Pacific region shows somewhat lower than expected growth than what we can see in the global data. What is very exciting is the growth of first-time guests.

This means not only great opportunities for spa and wellness centres but also service development challenges.

New guest segments, especially the younger generations, often have different expectations, and look for a different set of services and value propositions.

Owners, operators and developers would be advised to continually analyse both their current and future markets, which can often change rapidly, especially when it comes to international tourism markets.