One of the growing trends in the travel and hospitality sector is the rise of the wellness industry. With a greater focus on healthy habits and overall wellbeing, hotel spas are beginning to experience the positive impact of this trend. Within the UAE, Dubai’s spa market is in the lead, with more than 200 spas currently in operation, and more than 25 new hotel spas expected to open in the next year.

Given the growing significance of spas in the region and the interest from leading operators, Colliers International Hotels (MENA) launched the Dubai Spa Benchmark Report in 2015. The report features 14 key metrics designed to track spa operational performance.

Dubai Spa Market Performance

The 2016 market performance report is based on data received directly from a spa panel representing a stock of 321 treatment rooms.

Market performance in 2016 In 2015, the Dubai spa market experienced a 5 per cent decline in average treatment rates, due to increased pressure from new entrants and an increase in price-sensitive customers.

The rising popularity of spa and beauty apps offering promotions and discounts has also pushed up competition in the industry. However, 2016’s full-year figures reveal Dubai’s spa market has remained resilient. Average treatment rates grew by 5 per cent, from AED363 (US$99, €83, £75) in 2015 to AED382 (US$104, €87, £79) in 2016. Demand for treatments was steady – an average of 24 treatments per day in both 2015 and 2016. Overall, RevPATH (Revenue Per Available Treatment Hour) increased by 2 per cent in Dubai, indicating a small growth in spa revenues.

The largest share of demand in Dubai’s hotel spas is generated from the domestic market, representing 45-55 per cent of spa guests. Top source markets include GCC, UK and India, primarily those residing within the UAE. Demand for hotel spas has increased from UAE residents, with both city hotels and resorts reporting an increase in walk-in demand. International demand may represent anywhere between 20 and 40 per cent of guests, and is driven mainly by UK, German and Russian markets.

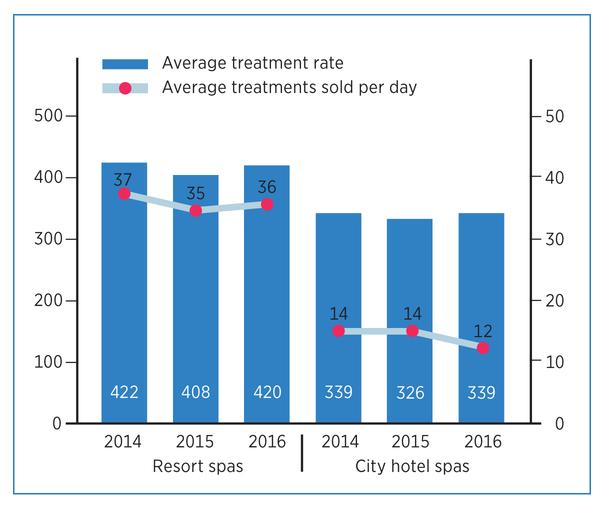

A closer analysis of the data reveals that the growth in spa revenue continues to be driven by Dubai’s resort market. Dubai’s resort spas have been able to recover from the dip in performance observed in 2015, returning to their 2014 performance levels.

Steady demand for resort spas

In 2016, resort spas in the sample demonstrated a slight growth in both rate and the number of treatments sold. Resort spas experienced a 3 per cent increase in average treatment rates from AED408 to AED420 (see Graph 2). The increase in average treatment rate is highest from Palm Jumeirah properties, a top-performing district within the Dubai hotel market in terms of hotel room average daily rate. Additionally, the average number of treatments sold per day in resort spas rose from 35 to 36 treatments per day. As a result, utilisation indicators have shown improvement, with an increase in both therapist and treatment room utilisation by 5 per cent and 9 per cent, respectively.

On the other hand, city hotels face challenges to maintain a steady customer base, as indicated by the drop in the number of treatments sold per day, from 14 to 12 treatments per day. However, city hotels experienced a growth in average treatment rate by 6 per cent, increasing from AED326 in 2015 to AED344 in 2016, resulting in a RevPATH growth of 2 per cent from AED43.6 to AED44.6.

While both resort spas and city hotel spas have seen an increase in the number of walk-in guests, resort spas have a higher share of in-house guests (61 per cent) than city hotel spas (57 per cent). As a result, resorts benefit from higher spending and bookings from tourists, while resident walk-in guests, often more price-sensitive, tend to look for discounts and seasonal promotions.

Retail revenue contribution showed a greater decline in city hotel spas than in resort spas (see Graph 1), falling from 11 per cent of total spa revenue in 2015 to 8 per cent in 2016. The data signals that hotels still cater to a higher share of price-sensitive demand, despite the rise in average treatment rates observed in 2016.

Increasing therapist productivity

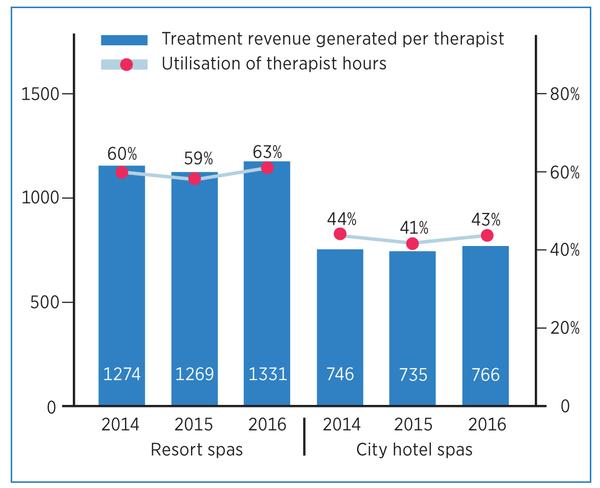

Therapist utilisation is an important indicator to ensure that a spa is correctly staffed. It’s calculated by dividing the available therapist hours for the given period by the occupied therapist hours.

Data from 2016 reveals that the utilisation of therapist hours has increased in both city and resort spas (see Graph 3). Therapist utilisation in city hotel spas increased from 41 per cent to 43 per cent in 2016, despite a decrease in treatments sold, suggesting greater efficiencies in staffing. Resort spas experienced a greater increase in therapist utilisation, from 59 per cent to 63 per cent in 2016, along with a 5 per cent increase in treatment revenue generated per therapist, resulting from an increase in the number of treatments sold per day.

Both resort and city hotel spas in the sample have an average therapist to treatment room ratio of 0.9; however, therapist utilisation rates are higher in resort spas than in city spas. Less than 50 per cent of therapists’ hours are currently utilised in city hotel spas, which indicates an opportunity to create greater operational efficiencies.

New spa openings

The Dubai spa market is continuously growing, with new competition entering the market. Anticipated spa openings in 2017 include the luxury Bulgari Hotels and Resorts, operated by Marriott International, in Q4 2017, and Ola Spa at the newly opened Lapita Hotel Dubai Parks & Resorts, plus many more.

When analysing the data by facility age, new spas (open less than five years) have a 10 per cent premium in rate over established spas (open more than five years), and an average of 28 treatments sold per day, compared to 21 treatments per day in established spas. However, therapist utilisation rates were 50 per cent in new spas versus 53 per cent in established spas, suggesting greater efficiencies in established spas. New spas have a higher capture rate (2.9 per cent versus 1.9 per cent) of hotel guests, which may explain the premium in rate new spas are able to achieve.

SURVEY: SPA PRE-OPENINGS

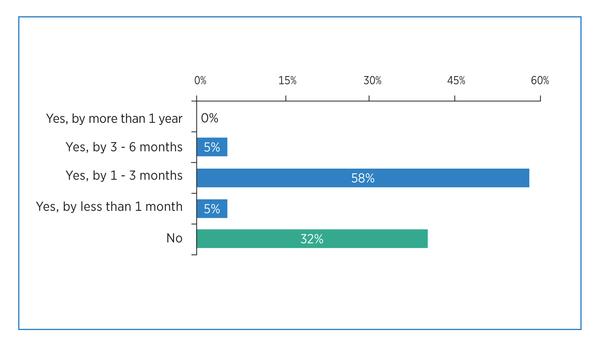

Given the large number of new spa openings in the Dubai hotel spa market, Colliers International conducted a survey in March 2017 on spa pre-openings. Results from 19 respondents revealed that 68 per cent of spa openings in the sample were delayed by between one and six months, out of which 58 per cent of respondents said the spa opening was delayed between one and three months.

The timeline to open a spa, like a hotel, requires extensive planning and execution. Often the time required to effectively open a spa is misjudged, leading to delays. The primary reasons for spa opening delays reported in the survey were a result of the hotel opening being delayed; delays in the delivery of furniture, fitting and equipment (FF&E), or FF&E not being up to brand standards; and issues with obtaining the necessary licenses and permits.

Only 13 per cent of the sample reported recruitment as a reason for spa opening delays. Spa directors were typically recruited 4.2 months before the planned opening, while spa therapists were hired an average 1.8 months before opening. Spa managers and supervisors were onboarded 2.6 months and 2.3 months before opening, respectively.

Training and marketing

Additionally, 84 per cent of the respondent spas had a soft opening, typically for a period of between one week to a month, giving staff time to be trained and to get accustomed to the spa’s operations. It’s vital for staff to be trained, tested and re-trained prior to the opening date, with an ideal training period of at least two to three months prior to opening. For many openings, training takes place at the last moment, which can negatively impact the reputation and perception of the spa right from the start. Spa directors would benefit from scheduling regular training sessions after the spa has opened to cover items the staff may have forgotten or missed.

The survey revealed that 58 per cent of respondents began marketing the spa one month or less before opening, with only 11 per cent of respondents beginning marketing from four to six months out. Given the highly competitive environment, it’s vital to get a viable sales and marketing plan in place during the pre-opening period, focusing on both in-house guest demand and domestic demand. Gift certificates, brochures, treatment menus and special spa packages should be developed well ahead of opening. It is critical to integrate the spa into all aspects of the hotel – from cross-selling by front office staff and concierge to in-room brochures and promotions. In this crowded marketplace, a smooth and timely pre-opening process is crucial to maximising financial and operational success.

Dubai spa market outlook

Once considered a luxury, wellness is now becoming part of everyday life – from how people work to how they travel. As the spa and wellness sector continues to grow in the region, hotel spas will have to innovate to adapt to demand from an increasingly price-sensitive customer base and competition from a constant stream of new entrants. Part of the innovation will require greater financial accountability of spas. Spa directors need to be able to accurately measure and consistently monitor the spa's performance and see how it compares to that of other spas within the market.