Collectively, the Gulf Cooperation Council (GCC) in the Middle East hosts 583 spas, according to the latest research from independent research company Intelligent Spas. In this part of the world, spas are booming and the region has one of the best open to closure ratios globally with 48 spas opening and only four closing since 2014.

The GCC is made up of the United Arab Emirates (UAE), Bahrain, Kuwait, Oman, Qatar and Saudi Arabia. For the purpose of the research, Intelligent Spas separately analysed Dubai and Abu Dhabi, the two largest spa markets in the UAE, and combined an analysis of the five other emirates which include Ajman, Fujairah, Ras al-Khaimah, Sharjah and Umm al-Quwain.

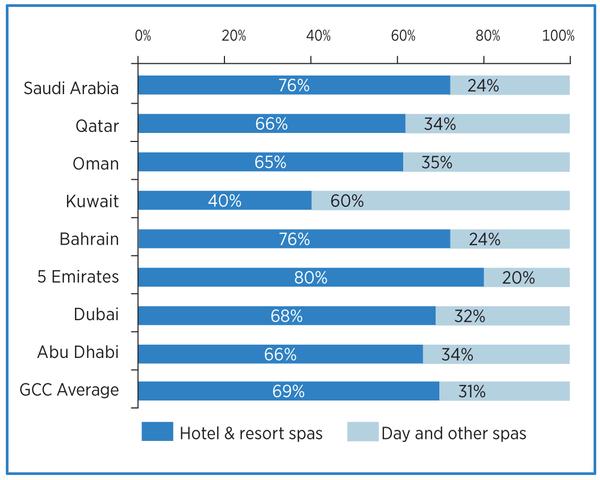

Out of all spas, 69 per cent are located in hotels and resorts in the GCC and 31 per cent are day spas, salon spas and other types of spas (see Table 1). The five emirates in the UAE, excluding Abu Dhabi and Dubai, collectively host the highest proportion of hotel and resort spas at 80 per cent, compared to Kuwait where 60 per cent of spas are day spas and other spa types (see Graph 1). What’s more, GCC spas are some of the biggest in the world:

• The indoor size of spas in the GCC region is 2,921sq m (31,436sq ft), compared to the global average of 1,781sq m (19,166sq ft)

• On average, they contain 9.9 treatment rooms whereas the global average is 8.9 treatment rooms

• Seventy-four per cent of spas promote public facilities for guests to use before and after treatments, compared to a global average of 49 per cent

• Forty-four per cent of spas with public facilities offer a plunge/spa pool, whereas 22 per cent offer a relaxation room

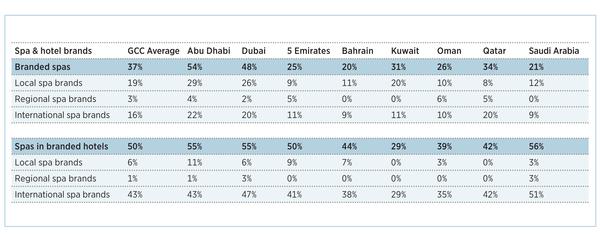

Branded vs individual

As part of the research, Intelligent Spas looked at spa and hotel brands in the GCC to identify the presence of regional and international operators. These findings provide some indication on how established and competitive each spa market is, suggesting what level the barriers to entry could be for a specific country/emirate, while providing an update on each chain’s market share for existing operators and industry stakeholders.

Intelligent Spas defines a brand as two or more spas or hotels using the same primary business name and operated by the same company. Local brands are those operating in the local or national marketplace, regional brands are those operating in multiple countries in the same region and international brands are those operating in more than one region. Looking at spas from this point of view, it’s possible to see that across the GCC:

• There are relatively few regional spa and hotel brands (see Table 2)

• On average, 37 per cent of spas are branded and 50 per cent of spas are located in branded hotels

• Abu Dhabi has the highest proportion of branded spas at 54 per cent, where 29 per cent of those are local spa brands and 22 per cent are international brands

• Fifty-six per cent of spas in Saudi Arabia are located in branded hotels, 51 per cent of which are internationally-branded. Meanwhile in Kuwait, 29 per cent of spas are situated in internationally-branded hotels

Development potential

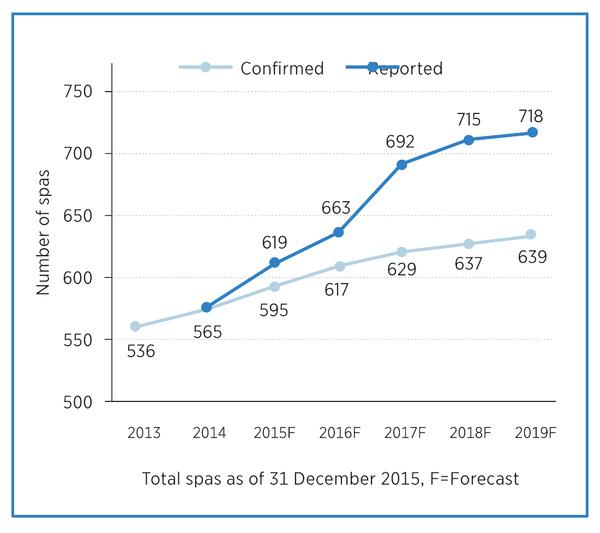

New spa development pipeline research conducted by Intelligent Spas identifies 139 proposed spa facilities that are due to enter the GCC between 2015 and 2019, potentially increasing the number of spas in the region by 27 per cent.

In comparison, confirmed developments over the same timeframe will see spa numbers increase to 639, up 19 per cent on those operating in 2013 (see Graph 2). Some other key findings of the spa development pipeline research included:

• The average size of confirmed spas under construction is 2,521sq m (27,134sq m) – 14 per cent smaller than the 2015 average

• The number of treatment rooms confirmed spa developments are planning is 13.1 on average – a 32 per cent increase on the 2015 average of 9.9 rooms

• Saudi Arabia has the highest industry growth potential, with spa numbers increasing by 53 per cent by 2018, if both confirmed and proposed developments are completed

• Oman’s spa industry is set to increase by 23 per cent between now and 2018, based on confirmed spa developments

• Dubai hosts the highest number of spas in the GCC, with over 190 currently operating and 34 more in the pipeline

Implications of the boom

While there are a handful of benchmark studies which look at spa performance in a select number of Middle East countries, this latest research by Intelligent Spas is one of the only studies to analyse the state of the spa sector in the region.

The overall outlook for the GCC spa industry is promising. But the fast growth will present challenges. New spas and more treatment rooms require more spa therapists, managers and directors. As there are a lot more spa openings than closures in the GCC, a shortage of qualified employees is predicted. With a reasonable proportion of spas located in international hotels and resorts, this will put pressure on the supply of both high quality therapists and experienced spa managers. The chains are better able to pull resources from other properties, however, individual operators could struggle and may need to introduce competitive compensation models to maintain high employee satisfaction and minimise staff turnover.

On the plus side, this will mean greater opportunities for training and educational institutions which are needed to supply newly certified and qualified employees to fill the HR gap. Product and equipment suppliers look set to benefit from the many new openings and refurbs (needed to maintain competitiveness) too. As do spa designers, architects and consultants who will be sourced to develop the new spas and guide the industry through all of these market changes.

The spa boom will also help raise the GCC’s tourism profile as each destination promotes its new, unique architecture and interior design, coupled with offering distinctive signature treatments based on local historical and cultural traditions.